2025 year in review

Reasons to remain cheerful

“The stock market is a device for transferring money from the impatient to the patient.”- Warren Buffett

From New Year’s Day 2022 to the bells of Christmas day last year, the price return from the FTSE 100 was less than that of being 100% invested in cash. Near 24 months and domestic equity prices could perform no better than a savings account. Fast forward just 11 months, the FTSE 100 has delivered a price return of 19% versus just 4% from cash. Add in dividends and the FTSE 100 has had a total return of +23.5% over this period.

Being patient with the UK has proved to be worthwhile, but being tactical has proved to be lucrative. Most wealth strategy funds within True Potential Portfolios turned more optimistic on the outlook for UK equities towards the end of 2024. This meant that managers added to UK equities and so boosted the returns delivered for clients over the last 12 months. Timing, in this instance, has proved to be perfect.

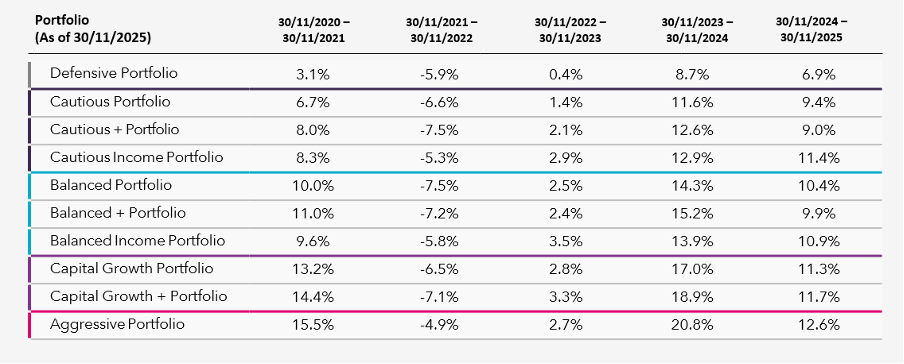

Source: True Potential Investments 30/11/2025. Net of Ongoing Charges Figure (OCF)

Performance is calculated on a Total Return basis and is net of Portfolio OCF. Performance information covers preceding 5 years and is based on complete 12-month periods.

Past performance is not a reliable indicator of future results.

It’s important to remember that, as with all investing, your capital is at risk. Investments can fluctuate in value and you may get back less than you invest.

Market drivers

Global equities look set to post their third successive double-digit annual return. And it is the FTSE 100 which has outperformed equivalents in both the US (S&P500) and Europe (Stoxx600) this year. Proof, if it was ever needed, that the stock market often behaves very different from the underlying economy. Recall that in 2024 the German equity index, the DAX, rose 22% despite the economy experiencing a modest recession.

Equity returns are being driven by several very identifiable factors:

- The first is a global boom in corporate capex, be it on AI infrastructure, software development or the utilities needed to generate and transport the energy required from this new ‘non-industrial’ age.

- The second is the ongoing level of government spending: the UK is likely to have run a fiscal deficit of 5% this year, France roughly the same and the US around 6%. Much of this government borrowing is being used to fund spending commitments, which helps keep economies ticking along.

- The third factor is a return to super normal profits of the global banking sector. The banking sector of both the UK and Europe has returned almost 70% this year. Banks are now benefitting from increased interest-margins, low loan write-offs and a détente in regulatory change.

Outlook

Once again, we can repeat the message that if the year ahead delivers even half the success of this year, then there is much to be optimistic about for True Potential clients. Inflation has peaked (again) in the UK and US, and this should allow both the Bank of England and the US Federal reserve to lower policy rates towards 3%. Stickier inflation in this cycle has proved to be the price of higher Government deficits and higher aggregate employment over this cycle.

Politics has proved to be a fly-in-the-ointment for portfolio returns. Markets have had a firm anchor in corporate capital expenditure and expanding margins. ‘Liberation Day’ tariffs imposed by US President Donald Trump initiated such volatility in equity markets that his administration began to roll-back on the rhetoric within weeks. Soft trade-deals with the UK, European Union, Japan et. al. soon followed. Now Trump is simply eliminating tariffs on most food imported into the US. France endured three different Prime Ministers in 2024 and onto their second this year – the current incumbent having also resigned just 4 weeks into the job, then being reappointed when no alternative could be found. The UK budget delivered far more noise than was necessary – perhaps we all would benefit from a return to an October fiscal event, rather than the sunset days of Autumn.

Looking ahead

All branches of the US Government are now back at their desks. By early 2026, the economic data flow will have returned to a regular cycle. The UK budget is now yesterday’s news. Market participants expect the Bank of England to continue cutting interest rates again. The balance-of-risks appears for the US Federal reserve to do the same, although any pause would be no big deal. The IMF and World bank have both upgraded their growth outlooks for 2026. Financial institutions such as JPMorgan and Morgan Stanley have recently done similar.

Monetary and fiscal stimulus is powering this optimistic outlook for the growth in corporate earnings and we share these sentiments entirely.

Sources: Bloomberg LLP

All figures as of 4th December, 2025

With investing, your capital is at risk. Investments can fluctuate in value and you may get back less than you invest.

This material is not a personal recommendation or financial advice and the investments referred to may not be suitable for all investors.

Opinions, interpretations and conclusions represent the views of True Potential Investments at the date of publication and are subject to change. Past performance is not a reliable indicator of future results.

Forecasts are not a reliable indicator of future results.

True Potential Investments LLP is authorised and regulated by the Financial Conduct Authority. FRN 527444. Registered in England and Wales as a Limited Liability Partnership No. OC356027.

True Potential LLP is registered in England and Wales as a Limited Liability Partnership No. OC380771.