Past performance is not a reliable indicator of future results.

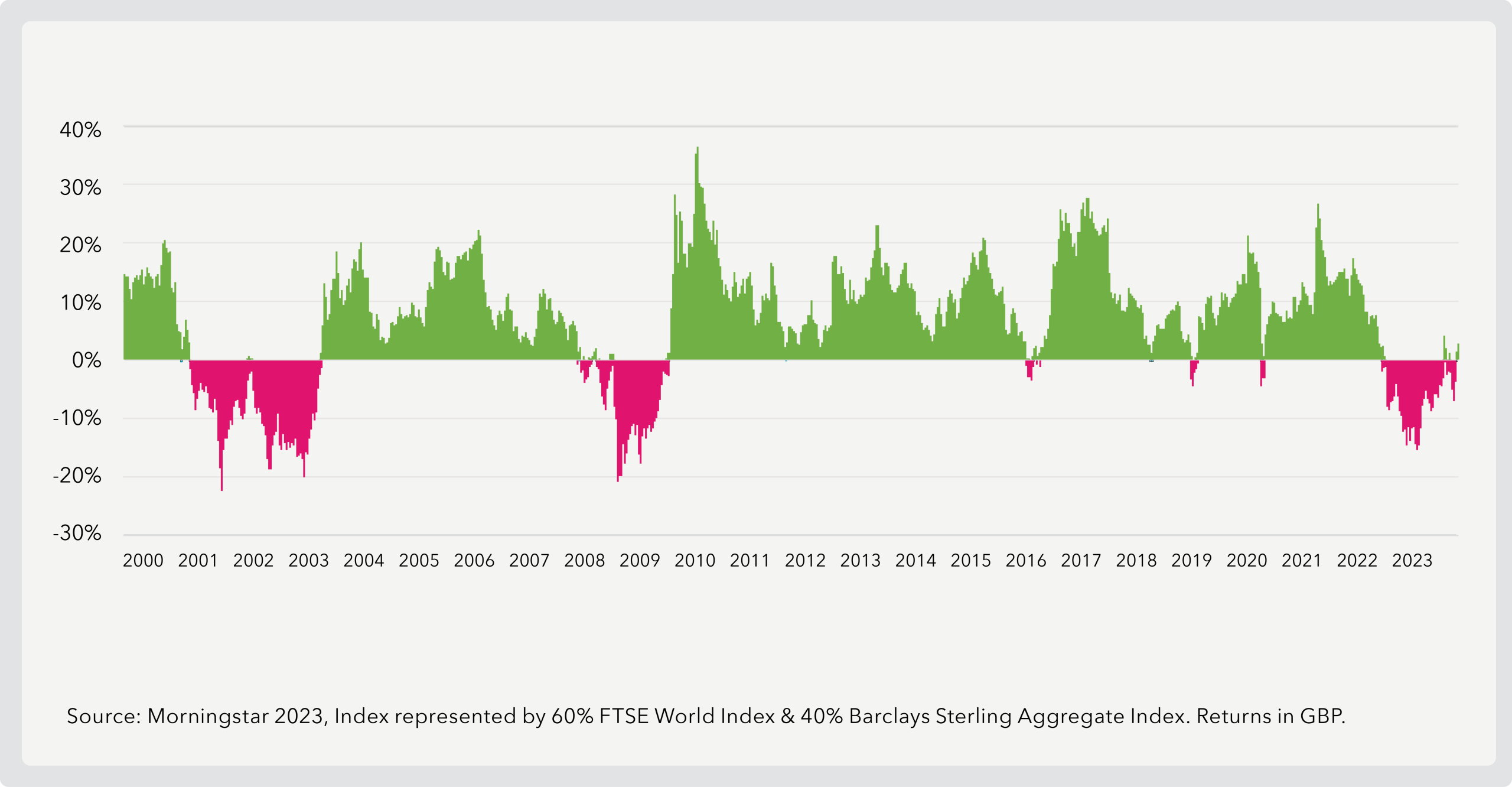

If we take the chart on a five year rolling basis, we can see that the positive returns have significantly shifted even more to 96% of the time.

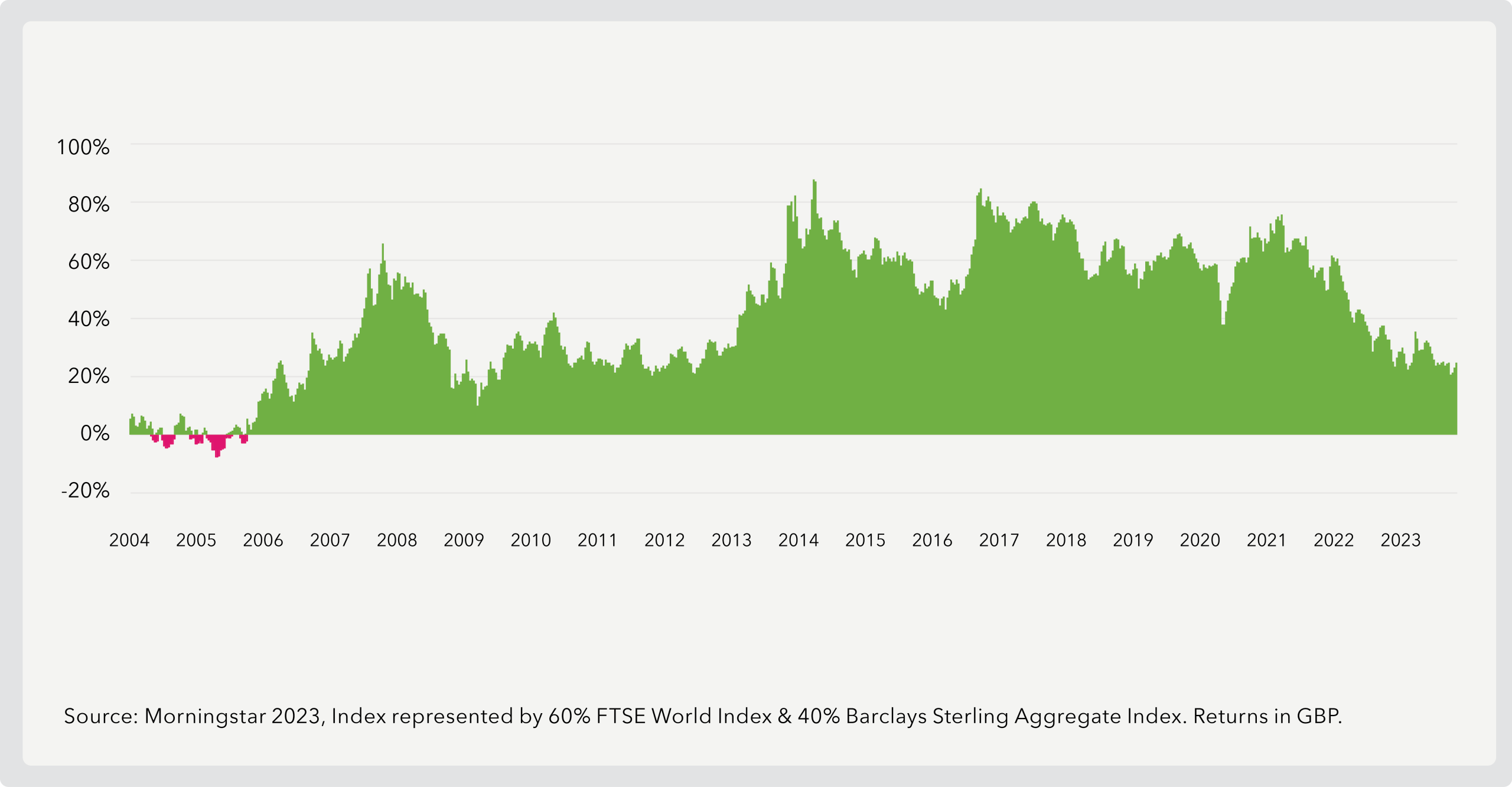

Over the past 24 years, unless you invested at the peak of the market of the dotcom bubble, you would have generated positive returns over five years. Through the financial crisis and through Covid-19 you would still be positive had you remained invested for five or more years.

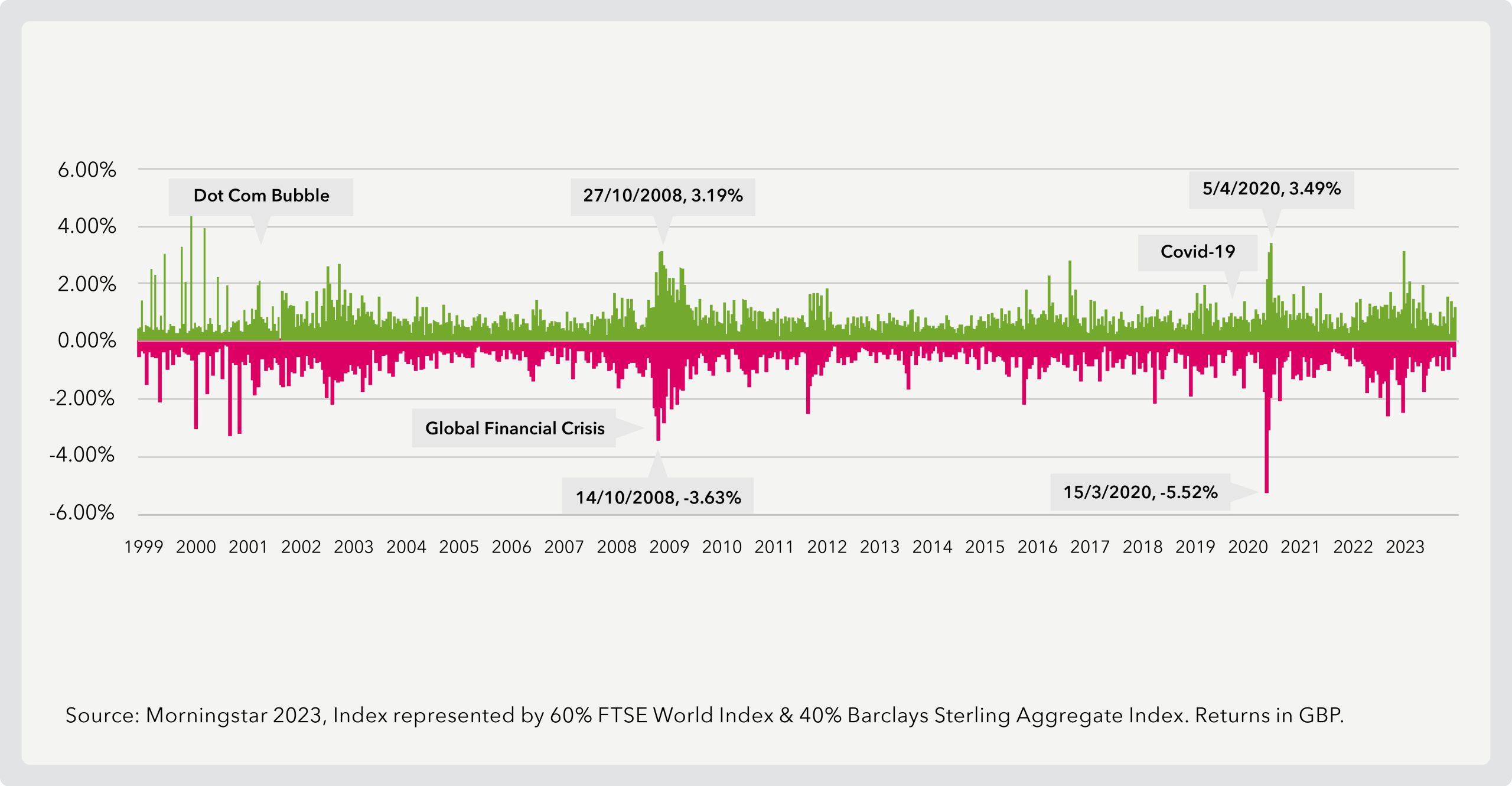

Not every year is going to be positive, we must understand that. If we look back over history, the events that have upset markets the most are the events that were a surprise. No one (or very few people) knew about them before the event happened.

It’s easy in hindsight to tell ourselves “we saw it coming, we should have done x,y,z” but in reality, everyone is on the same boat and no one will tell us what is over the horizon.

Hopefully, these charts highlight the risks of trying to time the market. The odds tell us all we need to know as we increase the period we look back over – from 50% positive on a daily basis to 80% positive yearly and even 96% over five years.

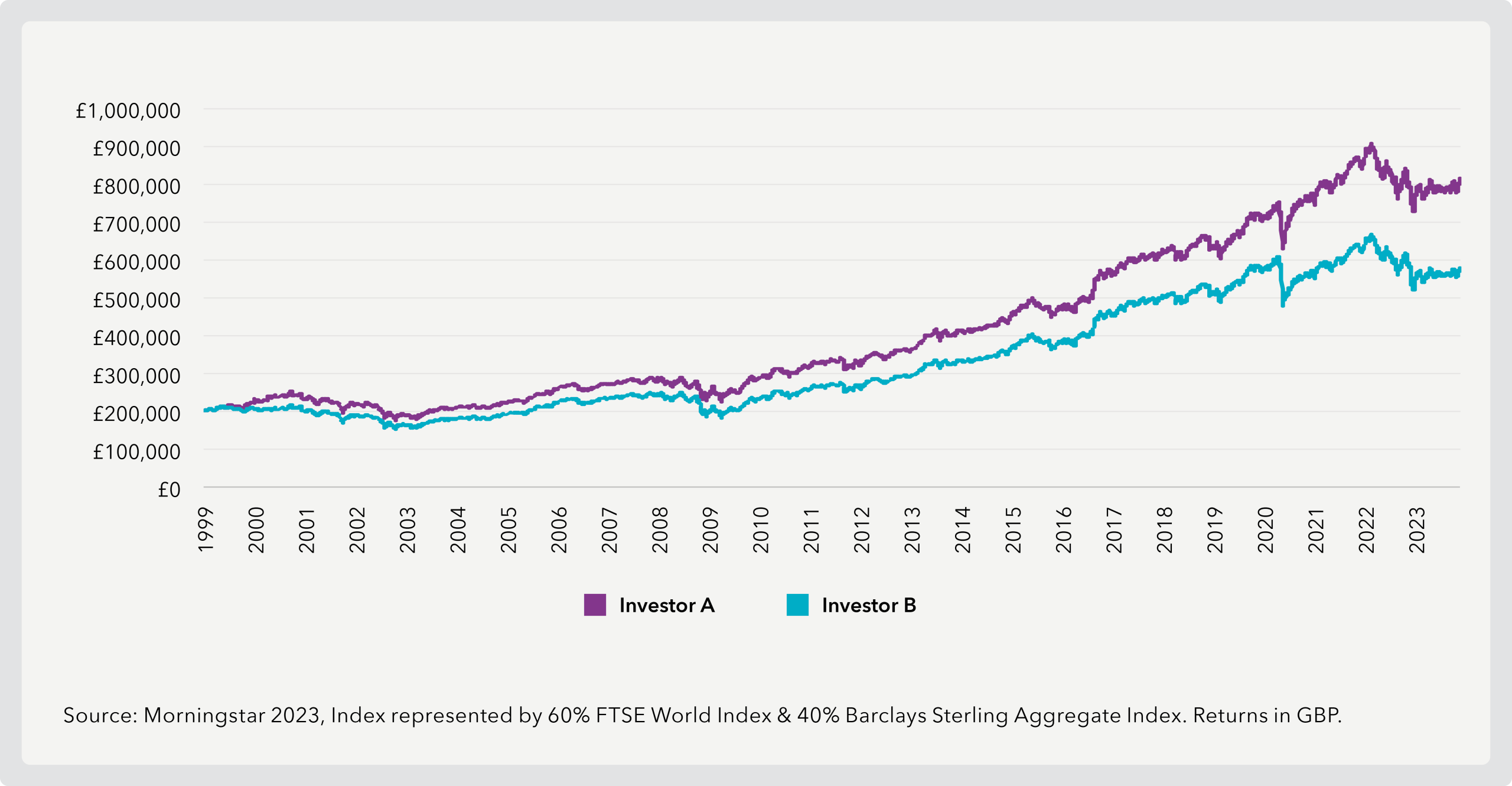

This shows us that to generate potential long-term returns, we should typically avoid making short-term shifts of investment strategies to disinvest and reinvest, other than when your overall attitude or capacity for investment risk changes.

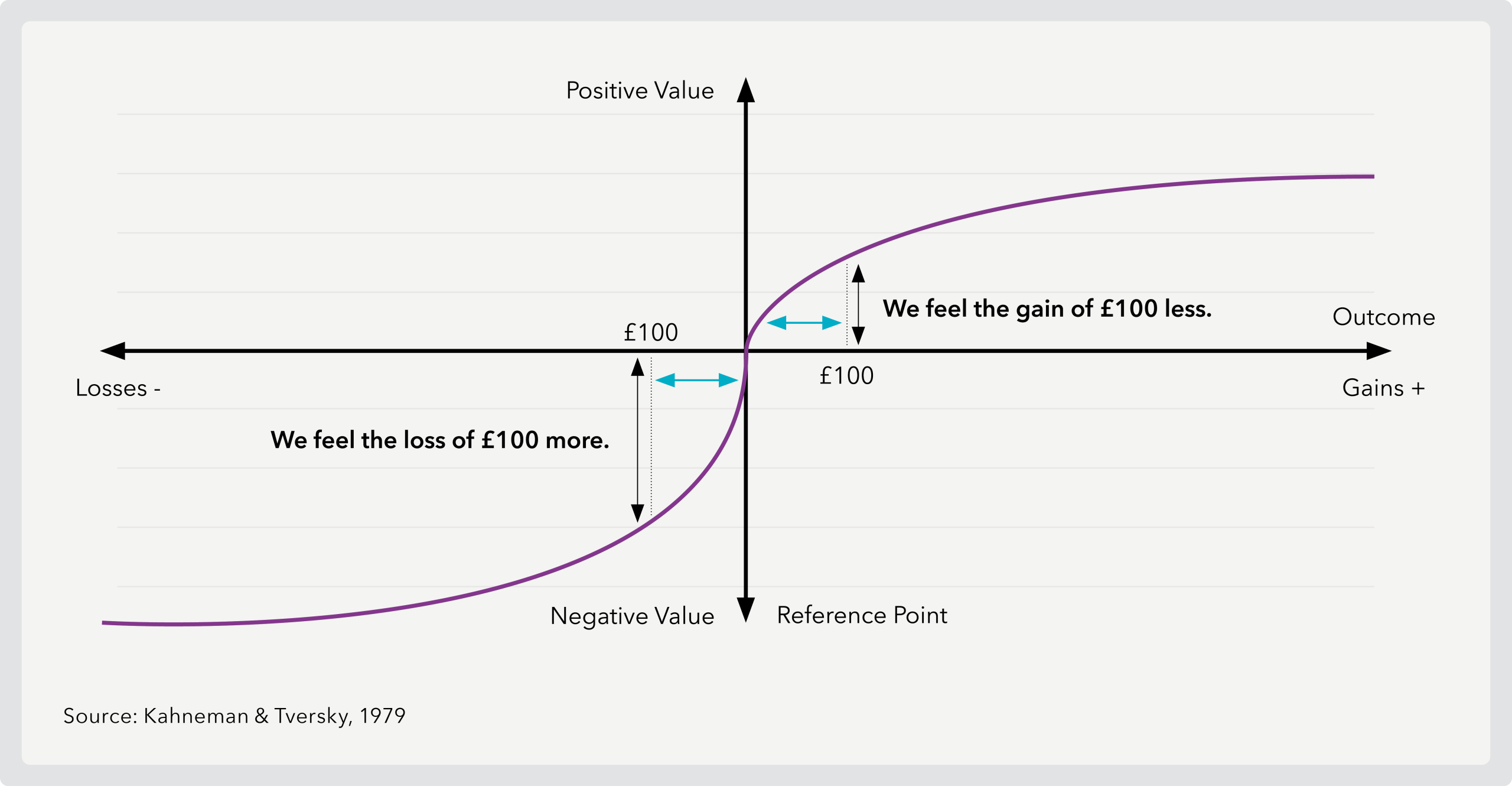

In terms of the psychology behind investing, these examples demonstrate how easy it can be to be influenced by market performance.

We can see that if investors are willing to take investment risk, remain disciplined and not allow decisions to be driven by fear and short-term volatility, it allows investors more opportunity to grow their wealth over the long-term.

This publication is not personal financial advice or a recommendation. If you are considering changing your investment strategy, it is important to get personal advice from a qualified financial adviser.

With investing, your capital is at risk. Investments can fluctuate in value and you may get back less than you invest. This material is not a personal recommendation or financial advice and the investments referred to may not be suitable for all investors.

Past performance is not a reliable indicator of future results.

True Potential Wealth Management is authorised and regulated by the Financial Conduct Authority. FRN 529810. Registered in England and Wales as a Limited Liability Partnership No. OC356611.

True Potential Investments LLP is authorised and regulated by the Financial Conduct Authority. FRN 527444. Registered in England and Wales as a Limited Liability Partnership No. OC356027.

True Potential LLP is registered in England and Wales as a Limited Liability Partnership No. OC380771.