An investment portfolio is one of the fundamental concepts of personal finance. It’s the name given to your collection of investments, which needs to be as strong as possible if it’s going to potentially help you reach your goals.

In this article, we’ll explain what an investment portfolio is in greater detail, as well as what makes a good one. Then we’ll walk you through the steps of how to build your own.

What is an investment portfolio?

An investment portfolio is a collection of financial assets owned by a single person or entity. It can include investments such as stocks, bonds and real estate, as well as funds like mutual funds and exchange-traded funds.

The term ‘portfolio’ comes from the Italian word portafoglio, which refers to a case for carrying loose papers. Although an investment portfolio isn’t a physical container, it could be helpful for you to think of it as something that holds all your separate investments together.

The goal of your investment portfolio is to build your wealth over time. Building and managing your portfolio are two of the key tasks of investing.

What can make a potentially good investment portfolio?

A good investment portfolio could be one that supports your financial goals, matches your risk tolerance and is diversified. There’s no one-size-fits-all solution, but understanding these different concepts can help you know if…

It matches your risk tolerance

Your risk tolerance is your willingness to risk losing money in exchange for the potential to earn greater returns.

From a practical point of view, your risk tolerance is connected to the timeframe of your financial goals. You might be able to afford to take on riskier strategies involving more volatile assets when investing for long-term goals (10+ years away), while a more conservative approach could be suitable if you only have a short time left until you’ll need your money.

Yet your risk tolerance is also about how you mentally handle the way financial markets – and the value of your investments – rise and fall. For example, it might be worth choosing a more conservative mix of investments if anxiety over losing money is going to prevent you from sleeping at night.

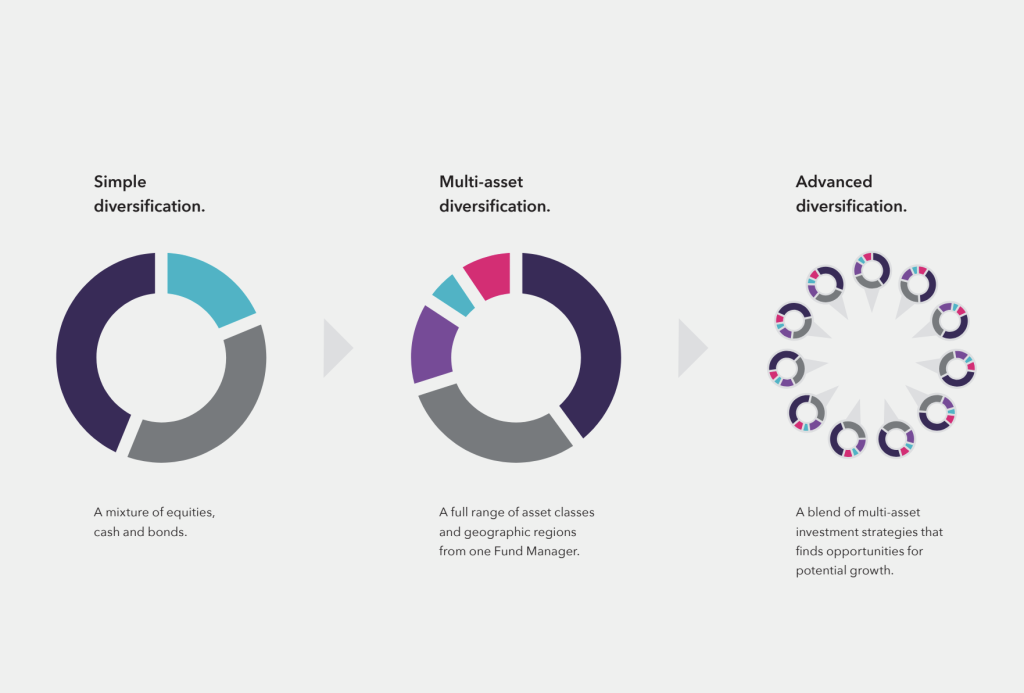

It’s properly diversified

Different investments are vulnerable to different risks. When the value of one asset is declining, the value of another may be on the rise. Diversification means holding a broad mix of investments to limit your overall exposure to risk, helping your portfolio to potentially continue growing under changing market scenarios.

One way to build a diversified investment portfolio is to spread your capital across different asset classes. However, you can also diversify within a single asset class. For example, by investing in company stocks in different industries or geographical locations.

True Potential Portfolios pioneer what we call Advanced Diversification, which means diversification through investment strategy, as well as assets. Different strategies behave differently to changing market conditions, so adapting a portfolio’s strategy can help make the most of opportunities and potentially mitigate risks .

Source context taken from page 10.

Image sourced from page 11

Image sourced from page 11

How to build an investment portfolio

The thought of building your own investment portfolio can be intimidating, and the truth is that it does require a certain level of time and expertise. Yet there are steps you can take to aid the process, depending on the level of involvement you want.

1. Decide how much help you want

It’s possible for you to build a potentially good investment portfolio from scratch. However, this requires considerable knowledge and effort to do properly; not everyone has the time and motivation for it.

You can get advice from our qualified financial experts if you want help figuring out which investments are right for you. They’ll take your financial goals and personal risk tolerance into account and help you build a diversified portfolio that may assist in reaching your goals. Alternatively, they can help you pick the most suitable option from a selection of ready-made portfolios.

2. Open an investment account

One type of investment account in the UK is a stocks and shares ISA (individual savings account). This is a tax-efficient account that lets you protect up to £20,000 from Income and Capital Gains Tax each year.

We offer a Stocks and Shares ISA, as well as a General Investment Account for those who want to invest beyond their ISA allowance. Our investment accounts give you access to personal financial advice whenever you need it and our award-winning platform lets you track your money 24/7. We also have simple and transparent fees that offer you value for money.

[Open an Investment account with True Potential]

3. Choose your investments

Once you’ve opened your investment account, you’ll need to fill it with assets you want to invest in. Common types of assets include:

- Stocks: Parts of companies that give you a share in their financial performance, either through price rises or dividend payments.

- Bonds: Loans to companies or governments that are paid back with interest after a fixed term.

- Index funds: Funds designed to track the performance of a given market, giving your portfolio a limited degree of built-in diversification across a given asset class. They tend to have lower fees as they’re not actively managed by a financial expert.

- Mutual funds: Bundles of assets that give you access to a diversified portfolio that’s built and managed by a financial expert. Your money is pooled together with that of other investors and managed by the fund manager who aims to achieve stated financial objectives and takes a fee.

4. Find the right asset allocation

Your asset allocation is the way you balance your capital across different types of assets. This ratio is mostly determined by the timeframe for your goals and your risk tolerance. Some asset types like mutual funds already have set asset allocations.

Some example asset allocations are:

- Aggressive (85% stocks, 15% bonds): You may find this level of allocation could be an option if you have a high-risk tolerance and a long timeframe for your goals.

- Moderate (60% stocks, 40% bonds): You may wish to choose this allocation if you have a moderate risk tolerance and a medium timeframe for your goals.

- Conservative (30% stocks, 70% bonds): A more conservative approach could be an option if you have a low risk tolerance and a short timeframe for your goals.

Our range of ready-made True Potential Portfolios make finding the right balance of investments simple. Whether you prefer a Defensive or an Aggressive approach, you can rest assured that your portfolio boasts market-leading diversification, offering you potential for growth

5. Rebalance your portfolio

As the value of your investments rises and falls over time, you’ll find that your asset allocation changes. This means that you’ll need to rebalance your portfolio, buying some assets and selling others to get your allocation back on track.

One option is to rebalance your portfolio periodically, say every 6 months or year. Alternatively, you can also do it when the allocation of one of your asset classes rises or falls more than a predetermined amount, such as 5%.

The process of rebalancing your portfolio can be time-consuming and complicated. Having a financial expert do it for you is one of the practical advantages of investing in a ready-made fund.

Build an investment portfolio that helps you achieve your goals

Building and managing a diversified investment portfolio takes time and expertise. It’s possible to do it for yourself but it can be much simpler to invest in a ready-made portfolio and have financial experts manage it for you.

Feel free to get in touch with our certified financial experts if you want to find out more about True Potential’s range of investment portfolios. We’ll be happy to discuss how they can help you achieve your investing goals.

With investing, your capital is at risk. Investments can fluctuate in value, and you may get back less than you invest. This material is not a personal recommendation or financial advice and the investments referred to may not be suitable for all investors.

Tax is subject to an individual’s personal circumstances, and tax rules can change at any time. ISA eligibility and tax rules apply. You should ensure your contribution does not result in your total ISA contribution within the tax year exceeding £20,000.

This blog is for information only and is not personal financial advice.

Back to blog