Why the global outlook is improving for investors

- Global equities have had a positive start to 2026

- Value stocks are driving stock markets higher

- The real-world economy stands to benefit from software investment

- Business sentiment is now the highest since Q4, 2024

This remains an expensive market – an expensive market not to participate in, that is. Global equities are up +3.3% (US dollar terms) this year, and this is despite an unusually slow start for US stocks – the S&P500 up a mere +1.8%.

There is no doubting that equity valuations across the global technology sector remain rich, perhaps explaining the -0.9% return (US dollar terms) from growth stocks since our last update in early December. Yet, value stocks are up +9.0% (US dollar terms) over the same period, to the benefit of equity markets in the UK, Europe, Japan and Emerging Markets. Returns there have been between +7% to +12% since 1st December.

Fiscal choices and falling inflation shape the next phase

This economic cycle remains unusual – most G7 governments continue to take leave of their fiscally conservative senses and intend to expand fiscal deficits over the next 12 months. Only the UK is an outlier – determined as it is to reduce the public sector deficit by over-taxing the private sector. There is an upside, however. UK inflation should meet a cliff edge come April, as the effects from the 2025 increase in the National Living Wage drop out. CPI may very well decline to 2% in short order and stay around that level. Finally, the Bank of England are almost certain to follow with further reductions in Base rate as the Spring bluebells flower.

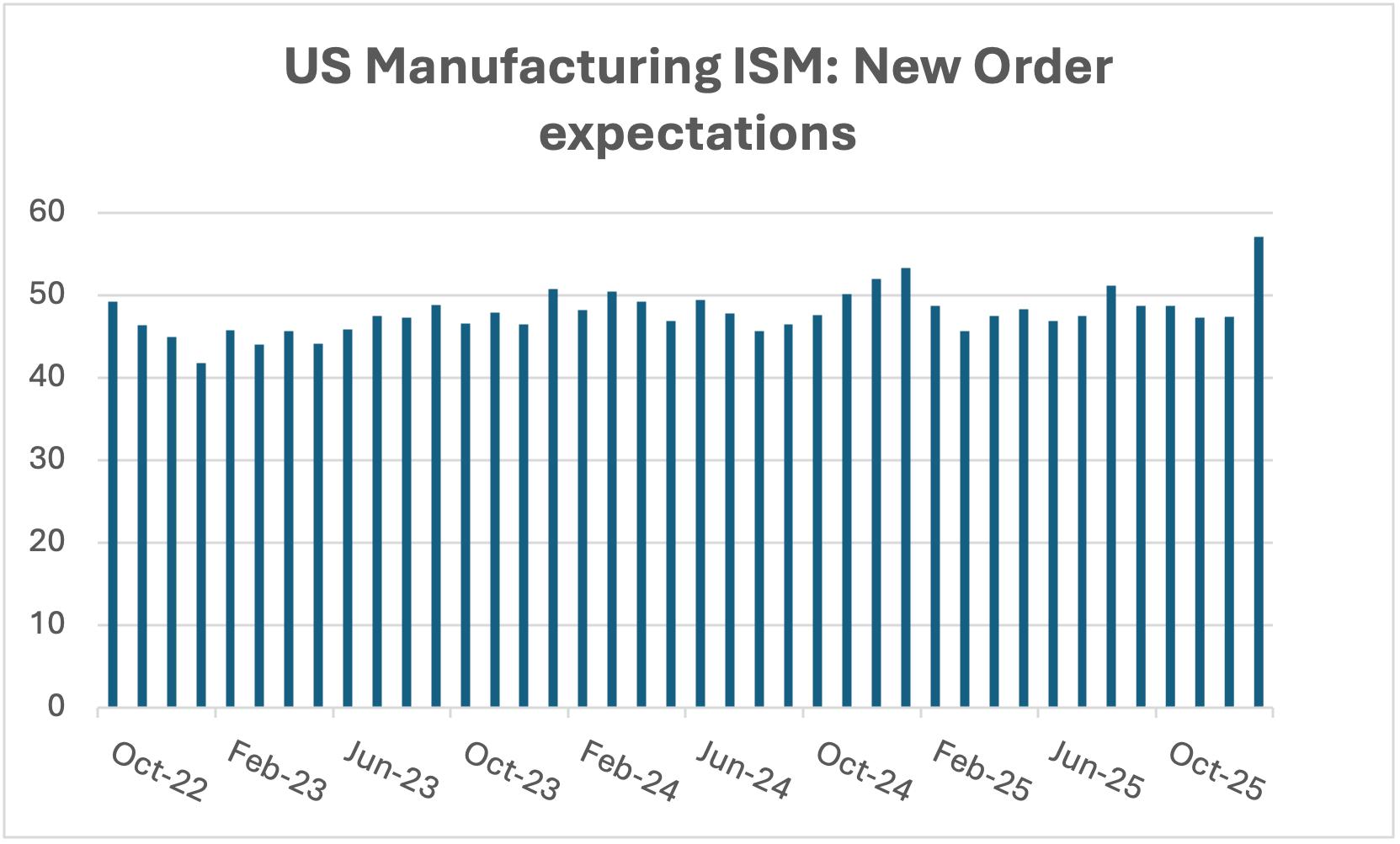

Global growth is shifting from software investment to the physical economy. In January, new order expectations within the US ISM Manufacturing survey jumped to their highest level in nearly 4 years.

Source: Bloomberg LLP

Source: Bloomberg LLP

The upswing is beginning to show in broader survey data – business activity sub-indices for both UK and US services economies climbed to their highest levels since October 2024 recently. Most of this can be explained by politics: the receding threat of further tax increases here in the UK, and a détente in Trump’s tariff war with the global economy. However, the starting point is one of near full employment and robust nominal growth.

Upside surprises in the global economy continue. The recent election of Japanese Prime Minister Takaichi with a parliamentary super-majority is encouraging and the ‘Nippon’ economy should continue its effervescent rise from prolonged deflation.

A constructive backdrop for diversified portfolios

For diversified portfolios, the market backdrop continues to hum. Volatility is here to stay, given the global political age we continue to endure, but worrying price swings are confined to crypto bets and precious metals. The former is an asset class for pure speculation (and grift) only, the latter a small part of any multi-asset portfolio.

Corporate profitability growth remains the bedrock of this cycle. Stay optimistic and stay invested.

All data sourced from Bloomberg L.P. (09/02/2026)

With investing, your capital is at risk. Investments can fluctuate in value and you may get back less than you invest.

This material is not a personal recommendation or financial advice and the investments referred to may not be suitable for all investors.

Opinions, interpretations and conclusions represent the views of True Potential Investments at the date of publication and are subject to change. Forecasts are not a reliable indicator of future results.

True Potential Investments LLP is authorised and regulated by the Financial Conduct Authority. FRN 527444. Registered in England and Wales as a Limited Liability Partnership No. OC356027.

True Potential LLP is registered in England and Wales as a Limited Liability Partnership No. OC380771.